https://cleartax.in/s/income-tax-officials-can-access-emails-social-media-accounts

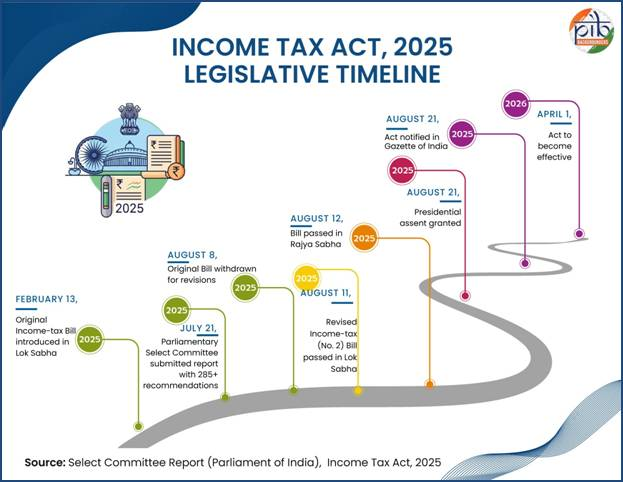

Section 247 of the Indian Income Tax Act, 2025 (which will come into effect from April 1, 2026) grants tax officials enhanced search and seizure powers, specifically extending their authority to virtual digital spaces like emails, social media, and cloud storage, in serious cases of suspected tax evasion.

Key Provisions of Section 247

- Expanded Scope: The law modernizes existing search powers (previously Section 132 of the 1961 Act) to include digital assets and records, reflecting the digitalization of financial transactions.

- Access to Digital Spaces: It defines “virtual digital space” broadly to include email servers, social media accounts, online banking/trading accounts, and remote servers.

- Mandatory Assistance: The provision mandates individuals to provide necessary technical assistance, including access codes and passwords, to enable officials to inspect digital records.

- Forced Access: It permits authorized officers to “override the access code” of any computer system or digital space if access is not provided.

- Targeted Use Only: Government clarifications emphasize that these powers are strictly limited to formal search and survey operations initiated due to credible evidence of significant tax evasion, and not for routine surveillance or normal assessments.

- Procedural Safeguards: The law retains procedural requirements such as the need for “reason to believe” that undisclosed income/assets exist and requires high-ranking official approval before a search can be conducted.

Concerns

The bill has raised privacy and ethical concerns due to the broad definition of “virtual digital space,” the power to bypass encryption, and a provision (Section 249) that bars the disclosure of the “reasons to believe” to the taxpayer, which some argue limits the ability to challenge the search in court. The government has stated it is developing standard operating procedures (SOPs) to ensure privacy and data integrity during digital searches.